Translate

Translate

AI Summary

- Ind AS 103 governs business combinations, requiring assets and liabilities to be recorded at fair value rather than book value for accurate financial reporting.

- Valuation under Ind AS 103 spans multiple stages, including identifiable assets, intangible assets, goodwill, liabilities assumed, and non-controlling interest (NCI).

- Intangible assets like brand names, customer relationships, and patents must be valued separately using methods like relief-from-royalty or multi-period excess earnings.

- Goodwill calculation depends entirely on fair value inputs, arising when purchase price exceeds net identifiable assets.

- Non-controlling interest valuation can use either fair value or proportionate share of net assets, while Ind AS 113 explains how valuation is performed.

In modern financial reporting, numbers are no longer just historical facts. They represent economic reality. Whenever one company acquires another, accounting is governed by Ind AS 103 – Business Combinations, and valuation becomes the backbone of the entire process because it does not only affect the initial recognition of assets and liabilities but also impact the future performance of the acquiring entity. In acquisitions, price paid ≠ book value.

Objective of Ind AS 103

Ind AS 103 ensures that when a business is acquired, the:

- Assets and liabilities are recorded at fair value

- Goodwill or bargain purchase is calculated correctly

- Financial statements show the true economic impact

Under Ind AS 103, accounting is done at fair value instead of book value. Hence valuation become most important aspect. IND AS 103 tells WHEN valuation is required and Ind AS 113 tells HOW to do valuation.

Where Valuation is Required under Ind AS 103

Under IND AS 103, Valuation is involved at multiple stages, its not a single step process. The key stages where valuation is required are as below: -

1. Identifiable Assets & Liabilities

At acquisition date, all identifiable assets and liabilities must be measured at fair value, including:

- Property, plant & equipment

- Intangible assets

- Financial instruments

- Contingent liabilities

Example:

A company buys another firm whose land book value = ₹10 crore But market value = ₹25 crore then Land must be recognised at ₹25 crore i.e. Fair value.

2. Intangible Assets Recognition

Even if not recorded earlier, these must be valued separately:

- Brand name

- Customer relationships

- Patents & technology

- Licenses

- Non-compete agreements

Example:

A company like Tata Consumer Products acquiring a beverage brand must value customer loyalty and brand strength separately.

Common Valuation Methods for Intangible assets can be:

- Relief-from-royalty method

- Multi-period excess earnings method

- Cost approach

3. Goodwill Calculation

Goodwill arises when purchase price > fair value of net assets. Goodwill is calculated as

- Consideration Paid

- Non-controlling Interest

- Fair value of previous holding- Net identifiable assets (Fair Value)

All the inputs used for calculation of Goodwill depends upon the valuation, hence it is purely a outcome of valuation.

4. Valuation of Liabilities Assumed

Under Ind AS 103, liability assumed must be measured at fair value when recognised. Liabilities assumed may include:

- Trade payables

- Provisions

- Contingent liabilities when criteria for recognition under Ind AS 103 have been met.

- Borrowings

- Liability of warranty

- Legal liabilities

- Liabilities related to unfavourable condition contracts.

- The need for valuation arises because the amount recorded in the acquiree’s books may not represent the actual obligation that you will presently incur.

For example:

- A long-term liability may need valuation on a present value basis, which would require all future cash outflows to be discounted to their present value.

- A warranty liability may need to be estimated based on the expected future cash outflows.

- A contingent liability may need to be determined using a probability adjusted fair value approach.

5. Valuation of Non-Controlling Interest

A non-controlling interest is the interest held by shareholders of the acquiree other than the acquirer where less than 100% of all outstanding shares are acquired. When measuring the NCI under Ind AS 103, there are two different approaches to measure NCI:

1. At fair value of NCI.

2. At the proportionate share of the identifiable net assets of the acquiree.

So why is there a need for NCI valuations? If the fair value method is used to measure the NCI at acquisition date, an independent valuation of the NCI itself is necessary. The independent valuation process may consider the following types of information depending on availability and the chosen valuation approach:

- Quoted market price of the acquiree's common shares, if available.

- Comparable company multiples for peer companies.

- Discounted cash flows from expected future operating profits.

- Minority discounts, if required based on facts and valuation approaches.

6. Valuation of Previously Held Equity Investment

When an acquirer has previously purchased some ownership interest in an acquiree through step acquisition (or cumulative acquisitions), that portion of the ownership interest may have a different value when control is acquired than it did at the date of the earlier purchase. Therefore, the previously owned equity interest must be valued at fair value as of the date of control acquisition.

Rationale for Valuation: The valuation of a previously held equity ownership interest will usually differ from the carrying value of the investment on the acquiring entity's financial statement when control is attained.

Main Valuation Methods Used under Ind AS 103

Valuation under Ind AS 103 is not based on a single method. Different assets and liabilities require different approaches. Broadly, the following valuation approaches are used.

Income approach

The valuation of an asset or a business using the Income Approach is primarily dependent upon establishing the present value of future economic benefits derived from that particular entity. The following methods can be used for determining an entity’s Value utilizing this approach:

a) Discounted Cash Flow Method: This approach is typically used to value, a business enterprise, shares, contingent consideration; a cash-generating asset. To value an entity utilizing the Discounted Cash Flow Method, the futurity of the entity’s expected cash flows is established and then discounted back to an appropriate present value based upon an established discount rate.

b) Multi-Period Excess Earnings Method: This approach is generally utilized to value, customer relationship(s), specific intangible asset(s). The value attributed to the entity via this method is determined after consideration has been given to both the residual cash flows generated from the entity’s business and from all contributory sources utilized by the entity to generate excess cash flows attributable to the asset being valued.

c) Relief from Royalty Method: This approach is typically utilized to value, brands, trademarks, trade names. The value derived from the entity under the relief from royalty methodology is determined by establishing a royalty or fee for the right to use an intangible asset as it would be provided via a third-party licensing arrangement.

d) With-and-Without Method: This approach is sometimes utilized to value, non-compete agreements, specific contractual rights. The value attributed to an entity under the with-and-without valuation approach is derived by contrasting the overall business valuation of that entity with the overall business valuation of the same entity but without the intangible assets being valued.

Market Approach

The Market Approach to valuing an asset or business is based on finding a value for the asset by finding other similar assets or businesses and determining their value through available market data. Common Methods for the Market Approach:

a) Multiples Derived from Comparable Companies can be used for business value, equity value, Nemesis Corporation, and examples of multiples include: EV / EBITDA, EV / Revenue, and Price / Earnings.

b) Multiples Derived from Comparable Transactions can be used when there are recent sales of similar companies or assets and may have been completed recently.

Cost Approach

The Cost Approach appraises an asset at its replacement or reproduction cost, taking into account depreciation and obsolescence. Common approaches include

a) Replacement Cost Method Appropriate for:

- Plant and Machinery

- Specialised Assets

- Technology/software

b) Depreciated Replacement Cost (DRC) If the asset is special and market data is not available.

Methods of Valuing Assets

The key value of an asset can be found through the following methods:

- Business Value – DCF/Market Multiple

- Shares issued as consideration – Market / DCF / NAV

- Brand / Trademark – Royalty relief

- Customer Relationships – MPEEM

- Technology – Income vs. Cost Approach

- Plant and Equipment – Replacement Cost / DRC

- Land / Building – Market Approach

- Compared Consideration – Weighted Probability DCF

- NCI = Comparable / DCF / Quoted Price if available.

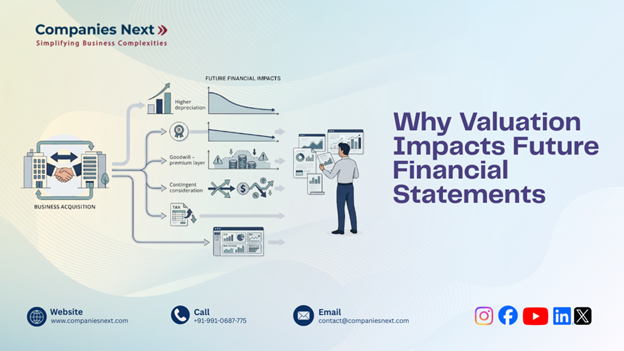

Why Valuation Impacts Future Financial Statements

The valuation process for Ind AS 103 takes place both at time of acquisition and over the course of time after acquisition. Future accounting implications include:

- Increased fixed asset fair value therefore increases depreciation expense.

- Recognizing finite-life intangibles creates amortization expense.

- Higher goodwill is likely to increase the chance of future impairments.

- Contingent consideration could create variance in profit/loss over time.

- The deferred taxes resulting from adjustments to fair values will impact tax expense after acquisition.

- Valuation assignments can also have an impact on segment profit and return ratios.

In summary, the decisions regarding valuation that you make at the time of acquisition will have an ongoing effect on the financial performance and statements throughout the future.

Conclusion

Although the way Ind AS 103 is presented looks like an accounting standard, by nature it is a valuation-based standard. The requirement to measure each asset acquired and each liability assumed at fair value leads to valuation being of prime importance to every key output of business combination accounting.

From the consideration transferred for a business combination to the measurement of the intangible assets acquired and the contingent liabilities assumed, to the determination of non-controlling interest, to the determination of impairment, goodwill, deferred taxes, and many other similar measurements, valuation impacts each of the significant measurements in the transaction. It will also affect depreciation, amortization, impairment, profit and disclosure, all of which will be reflected in the future.

The acquisition method requires a valuation to be undertaken for the acquisition to operate in a logical manner. The financial statements also will not appropriately reflect the true economics of the transaction should the valuation be unreliable. Valuation is truly the heartbeat of all business combination accounting under Ind AS 103.