Translate

Translate

AI Summary

- India taxation for foreign companies involves Corporate Income Tax, GST, and TDS, with foreign firms taxed only on India-related profits through a Permanent Establishment at 35% plus surcharge and cess.

- Foreign subsidiaries in India are taxed as domestic companies at 22%, while special income like royalty, interest, and technical fees can benefit from reduced DTAA rates.

- Transfer pricing rules require arm's length pricing, a transfer pricing study, and Form 3CEB filing between foreign parents and Indian subsidiaries.

- GST registration for foreign companies applies to goods, services, digital sales, and events, with Non-Resident, OIDAR, and Regular options.

- TDS on payments to foreign businesses can be lowered using TRC, Form 10F, and no-PE certificates under DTAA benefits.

Today, India is one of the fastest-growing business destinations in the world. For expansion Global companies are setting up offices, selling digital services, opening subsidiaries, and partnering with Indian firms. It is necessary to understand Indian taxation for foreign companies to reduce compliance burden and enhance profitability.

Unlike many countries, India has multiple tax systems working together:

• Corporate Income Tax

• GST (Indirect Tax)

• TDS (Withholding Tax)

1. Corporate Taxation on Foreign Companies

In India foreign companies are taxed only on profit earned in India. If foreign company is operating through permanent establishment in India only in that case foreign companies will be taxed in India.

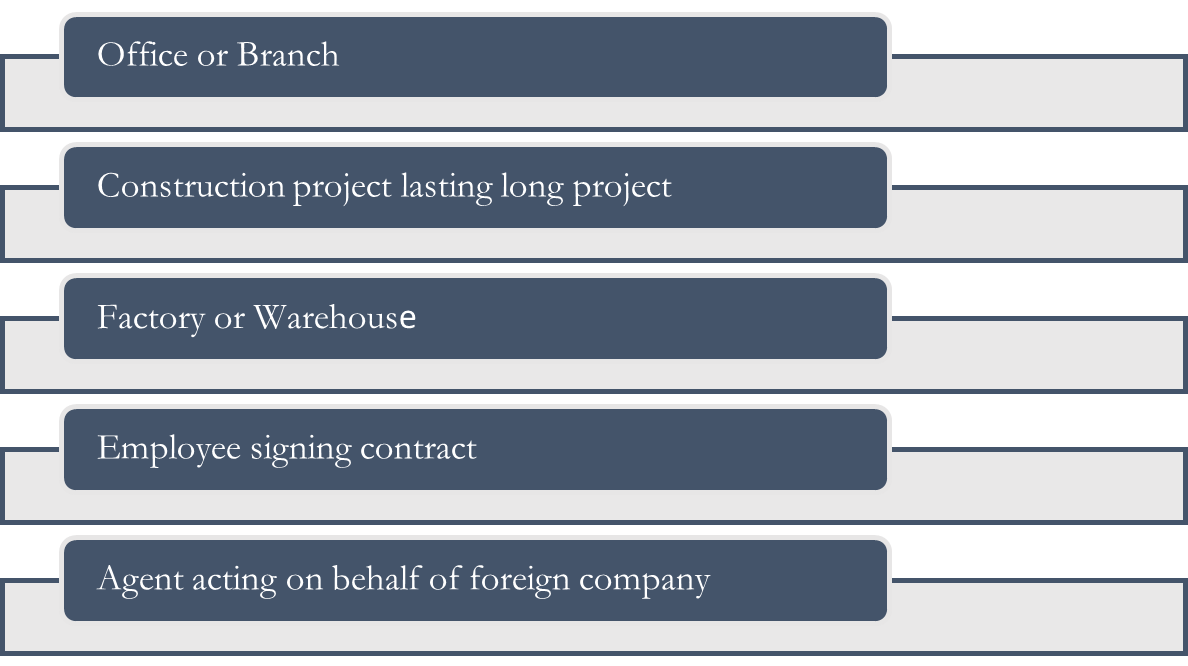

What is Permanent Establishment?

A Permanent Establishment means a real business presence in India, such as:

Tax Rate for business profits of Foreign Companies

- If a Foreign company has a PE or branch in India, only its India Related profits are taxed at the rate 35% + surcharge + cess.

- If Foreign company has established a subsidiary company in India, it will be taxed as domestic company at the rate of 22% plus surcharge plus cess.

Tax rates for other types of income

Foreign companies also earns income through various other sources such as dividends, royalty, fees for technical services. Income tax act, 1961 specifies specials tax rates for this income, which can be reduced with the help of DTAA’s signed between India and various countries. Summary of tax rates on special income earned by foreign companies are as below:-

|

Income Type |

Tax Rate as per Income tax Act, 1961 |

Tax Rates as per DTAA |

|

Royalty |

20% |

10-15% |

|

Technical Service Fees |

20% |

10-15% |

|

Interest |

20% |

10-15% |

Transfer pricing rules

If foreign parent company deals with Indian subsidiary, price must be at arm’s length price according to the rules.

Companies must file:

- Transfer pricing study containing complete documentation regarding calculation of Arm Length price.

- Form 3CEB.

2. GST For Foreign Companies:

India’s indirect tax system is called Goods and Services Tax (GST) which is applicable on It is necessary to understand GST provisions as it

GST Registration Must Be Done If:

- It sells goods in India.

- It provides services from India.

- It participates in exhibits or events.

- It sells digital services to Indian consumers.

There are 3 types of registrations a foreign company can obtain depending upon there mode of operations. It has been summarized as below:-

|

Type of Registration |

When Required |

Key Features |

|

Non-Resident taxable person |

Occasional supply of Goods and Services in India |

Registration for Limited period (90 days + 90 days Extendable) |

|

Online Information & Database Access or Retrieval services |

Tax payable only on supplies to unregistered person |

|

|

Regular registration |

If operated through fixed place of business in India (Subsidiary company/LLP) |

Works as normal registration, Input tax credits allowed |

Once registered every foreign company must comply with

- Monthly fillings

- Collect and make tax payment

- Maintain proper records and tax invoices

3. TDS On Payments to Foreign Businesses:

TDS means tax deducted at source. Foreign companies receiving payments from Indian customers may be subject to TDS depending upon the nature of services provided. TDS is generally deducted based on tax rate as per Income tax act, 1961. However foreign companies can provide various documents such as TRC, Form 10F and no PE certificate to claim benefits of DTAA’s and subject to lower TDS rates.

Foreign companies can claim the credits of TDS deducted on payment while filling their Income tax returns. Income tax also offer lower TDS deduction certificate in various cases to stop blocking of funds deducted as TDS.

Common TDS rates are as follows:

|

Payment Type |

TDS rates as per Income Tax Act,1961 |

TDS rates as per DTAA |

|

Royalty |

20% |

10%- 15% depending upon residency of Foreign Company |

|

Technical Fees |

20% |

10%- 15% depending upon residency of Foreign Company |

|

Interest |

20% |

10%- 15% depending upon residency of Foreign Company |

|

Dividend |

20% |

10%- 15% depending upon residency of Foreign Company |

How to Utilize DTAA: India has a vast number of countries that have entered into Tax Treaties with over 90 countries, which provide for reduced TDS in cases of TDS generated from foreign businesses to Indian businesses.

To apply the reduced TDS rate, the foreign business must have a Tax Residency Certificate and Form 10F.

4. Equalisation Levy (Digital Tax):

India introduced Equalisation Levy to tax digital income earned by foreign companies from Indian customers. The levy was introduced under the Finance Act, 2016 and currently applies in two different situations, each with a separate rate.

- 6% Equalisation Levy – Online Advertisement Services

- 2% Equalisation Levy – E-Commerce Supply or Services

5. Common Tax Mistakes Made by Foreign Companies:

- Opening office without tax planning

- Ignoring GST on digital services

- Wrong TDS rate

- Not using tax treaty

- No transfer pricing documentation

- Late filing

Any of the above can result in penalties and receive notices from the tax authorities.

Conclusion:

Entering India without tax planning is like starting a journey without a map. Corporate tax rates, GST registrations, TDS deductions, Equalisation Levy rules, and FEMA regulations all work together to define how foreign companies operate here. The laws are detailed, but they are clear once understood.

Foreign companies that study the rules, structure operations properly, and stay compliant under Indian tax laws avoid surprises and build long-term success.

Because in India, good tax planning is not about paying less tax—it is about doing business with confidence.